Pervading Factors Behind Floating Solar Power Gridlock in Indonesia

By: Anya Azaria & Rikordias Siahaan

Report Content:

I. Introduction

II. Policy and Regulation

III. Licensing

IV. Issues & Challenges of Developing Floating Solar Power Plant in Indonesia

V. Opportunities in Indonesia

VI. Existing and Planned Floating Solar Power Plants in Indonesia

VII. Industry Contacts

I. Introduction

Indonesia has quite a large potential of solar energy, reaching 400,000 MWp or equivalent to 400 GWp. According to the Indonesian Government (Directorate General of New, Renewable Energy MEMR) in 2022, the total installed capacity of solar power plants (PLTS) was only 432.6 MW. However, based on the 2021-2030 Electricity Supply Business Plan (RUPTL) of state-owned electricity firm PT PLN, new PLTS capacity development is targeted at 4.7 GW to help achieve the government’s target for new and renewable energy (EBT) to account for 23 percent of the country’s energy mix in 2025. This shows that Indonesia is still far from achieving this target. Based on the RUPTL 2021-2030, PLTS contributes 22.4 percent of the total renewable energy development plan. To reach the EBT target of 23 percent in 2025, the government is also pushing the development of PLTS in several locations, such as in ex-mining areas which have a potential capacity of 435.5 MW, in dam areas which have a potential capacity of 612 MW, and in PLN’s existing power plants which have a potential capacity of 112.5 MW. In this report, we focus on the PLTS development in dam areas in Indonesia.

Solar power plant development can be done in various locations. It can be implemented on land (ground-mounted), roof (rooftop), and also on the water (floating). One of the obstacles in the development of solar power plants is the huge land requirement. If it is a ground-mounted type, the available land is mostly located in areas with small population and little electricity demand. Conversely, narrow land is in a location with a dense population, so the potential area for developing solar power plants is quite low. In addition, not all roofs can be fitted with solar power plants, so we see great potential for massive solar power plant development, especially through floating solar power plant (FSPP) development.¬

.jpg)

FSPP is a large-scale solar module system that is installed floating on a platform on the surface of the water, whether in a lake, reservoir, dam, irrigation lake, wastewater management area (water treatment pond), or offshore. In this report, we focus on the development of FSPP in dams which are managed by the Ministry of Public Works and Housing (PUPR). In general, FSPP is not much different from ground-mounted systems. FSPP consists of solar modules, floating platform/floater/pontoon, mooring system, inverter, power conditioning station (on land or water), cabling, network interconnection infrastructure, supporting facilities, meteorological center, remote monitoring, and data collection system. After we look at the introduction, now we examine the policy and regulation that oversees FSPP in Indonesia.

II. Policy and Regulation

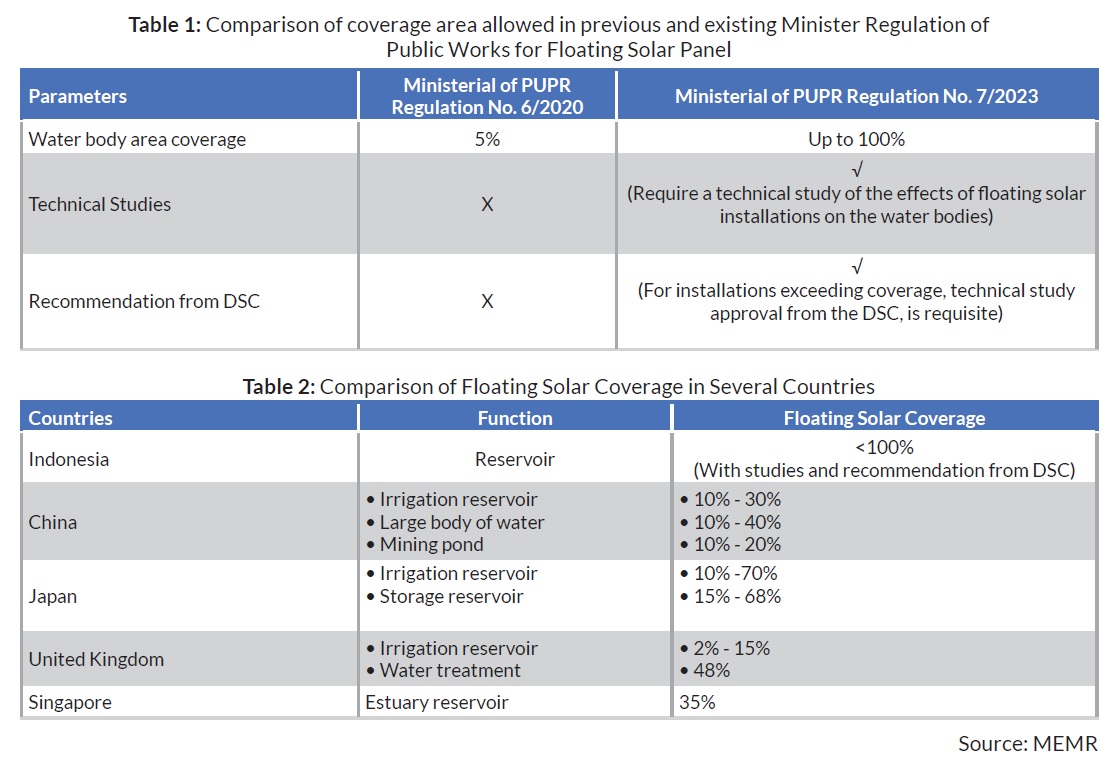

The most notable regulation on FSPP is Regulation of Minister of Public Works number 7 Year 2023, which sets the allowance of coverage area of dams for FSPP. Based on this latest regulation, developers have the freedom to utilize up to 100 percent of the total area of the dam for FSPP development, whereas in the previous regulation it was limited to only 5 percent. For the record, if the coverage exceeds 20 percent of the total area, the developer is required to carry out a feasibility study (FS) supplemented by recommendations from the Dam Safety Committee (DSC).

When compared with other countries such as China, Japan, the United Kingdom, and Singapore, which on average can utilize around 10 percent to 70 percent of the reservoir area, Indonesia has managed to excel with regulations that can utilize 100 percent of the reservoir area (summarized in Table 2). After learning the regulations that govern floating solar power plant development, we now look at the licenses that are needed to develop FSPP in Indonesia.

III. Licensing

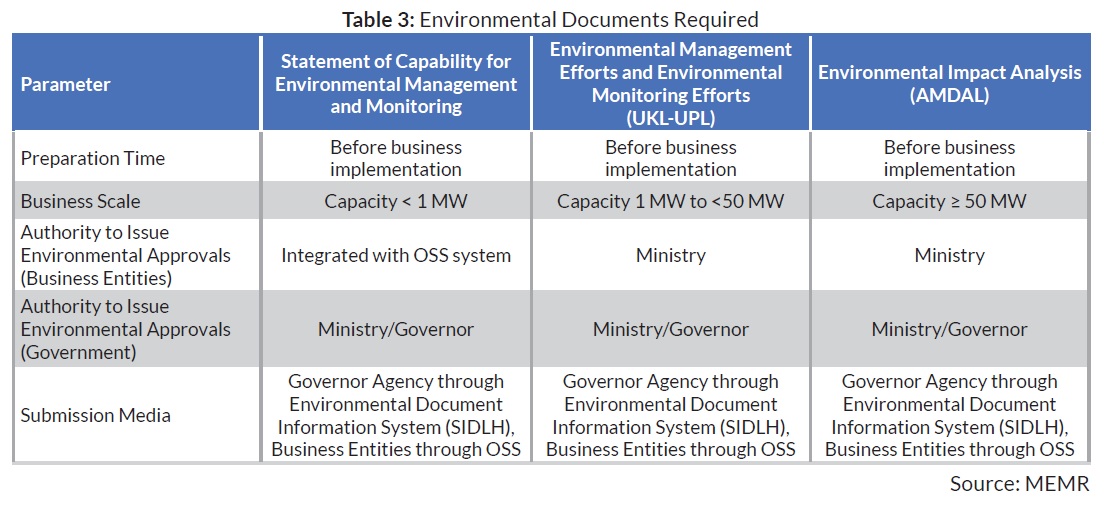

There are several important licensing requirements for developing FSPP in Indonesia, namely reservoir access permit, environmental approval, water resources utilization permit (IPSDA), building permit (IMB), borrow and use forest areas approval (PPKH), and electricity permit. These six permits can be processed separately, but the environmental permit needs to be processed first as a basis for processing other permits.

III.1 Reservoir Access Permit

Permitting the use of access to dam areas or water bodies depends on the status ownership of each reservoir or water body. Licensing can be processed based on two ownership classifications:

- Private ownership, including ownership by State-Owned Enterprises (BUMN). The licensing that needs to be done is relatively simpler with a Business to Business (B2B) scheme between prospective FSPP developers and owners of dams or water bodies.

- Government ownership. Compared to private ownership, the licensing process for government-owned water bodies is more complex and involves more stakeholders, such as the Ministry of Finance, and involves regulations related to Government and Business Entity Cooperation (KPBU).

III.2 Environmental Permit

Environmental approval is a permit that needs to be processed first before processing other permits. Environmental approval issued in the name of the company submitting the Environmental Impact Analysis (AMDAL) application. If the prospective location for the FSPP is located in one district area, the permit is submitted to the District Government. For areas located in more than one district, permits are required to be submitted to the agency responsible for the environment at the provincial level.

III.3 Water Resources Utilization Permit (IPSDA)

IPSDA is required if the project being carried out falls into the business category of water resources and is required before the construction process can be carried out. IPSDA applies like Building Construction Permit (IMB) for water areas. IPSDA is issued by the Directorate General of Natural Resources-Ministry of PUPR. IPSDA is required for financing dates with PT PLN (Persero) and financing disbursement with lenders.

The IPSDA management process consists of several stages, which are document preparation, process technical recommendations, and processes by the Director General of Natural Resources-Ministry of PUPR. Business entities coordinate with the River Basin Center (BBWS), regarding the need for recommendations techniques by BBWS. Design approval and construction permits are issued by BBWS-PUPR with submitted Detailed Engineering Design (DED) documents. Then, the business entity submits a recommendation request technique to BBWS. If technical recommendations have been issued by BBWS, the next process is evaluation carried out by BBWS. After that, the permit is processed by Dit. Development of OP Directorate General of SDA-Ministry of PUPR.

III.4. Building Permit (IMB)

In several areas, FSPP has not become an IMB object and has been replaced by IPSDA as an IMB for water bodies. However, IMB is still required for components and supporting infrastructure at the edge of the body of water. Licensing can be done through the One Stop Integrated Service of the respective District Service location.

III.5 Borrow and Use Forest Areas Approval (PPKH)

PPKH is submitted to the Ministry of Environment and Forestry (KLHK) based on recommendations from the local Governor and the Indonesian State Forestry Corporation (Perhutani).

III.6 Electricity Permit

There are several requirements for the application of a Business License for Providing Electricity for Public Use (IUPTLU). The first is a feasibility study for the electricity supply business which contains a financial feasibility study, operational feasibility study, network interconnection study, installation location, one line diagram, business type and capacity, development schedule, and operating schedule. The second is an electric power sale and purchase agreement between the applicant and the prospective electric power buyer following the provisions on the selling price of electric power or has received approval from the Minister or Governor by the authority.

After knowing the licenses that are needed to build FSPP, we will now look at the price of electricity produced by FSPP, assuming the power is to be sold to PLN.

.jpg)

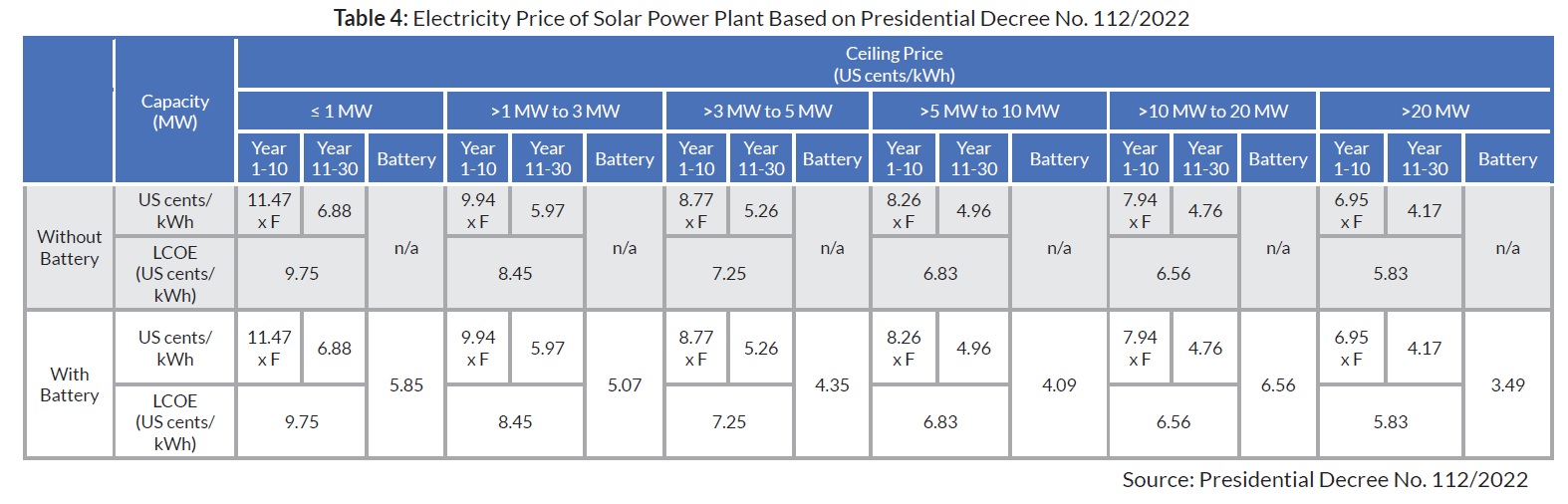

IV. Pricing

Assuming that the electricity produced from FSPP is to be sold to PT PLN (as Independent Power Producer), then we need to look at regulations that manage the selling price and mechanism to do so.

Referring to Presidential Decree No. 112/2022 concerning the Acceleration of Renewable Energy Development for the Supply of Electric Power, Table 4 shows the ceiling price (HPT) of solar power plant both using batteries and not using batteries of which FSPP is included as solar power plant, to PT PLN. Meanwhile, Table 5 shows the location factor (F) used to calculate HPT at the first stage (first year to tenth year).

V. Issues & Challenges of Developing FSPP in Indonesia

Even though Solar PV clearly has advantages in terms of price, especially in locations that have high irradiation, in Indonesia, the development of Solar PV has been hampered, especially by regulations. The section below describes what issues are hampering the development of Solar PV in Indonesia.

V. 1 Monopoly of power market

The relatively large amount of power generated from floating solar power plants will be more efficient if it is also sold to other parties and not only consumed by itself. Therefore, the floating solar power plant utilization scheme model would be better served by IPP or private utility. Allowing the market to work in renewable energy development, including in solar power is essential for two main reasons, among others; efficiency and innovation.

Markets are driven by supply and demand, which naturally encourages the allocation of resources to where they are needed most. When left to the market, renewable energy projects that are the most economically viable and efficient tend to be prioritized. This promotes resource optimization and cost-effectiveness.

Market competition spurs innovation. When businesses and entrepreneurs compete for market share, they are incentivized to create more efficient, cheaper, and environmentally friendly renewable energy technologies. This competition can lead to breakthroughs that benefit society, something at floating solar power will fit into perfectly.

Limiting private sectors to develop floating solar power as in IPP, Private Utility or Own Use, is certainly barred Indonesia to reach its environmental targets in emission reduction.

- The Difficulty of Being a Private Utility

Becoming a power utility in Indonesia, like any other industry, has its share of challenges and potential unattractive aspects. To become an independent power utility in Indonesia, the first thing that must be obtained is an electricity business area (or a concession). To obtain a business area for power utility, there are certain requirements that must be fulfilled. One of them is for PLN to return the desired area to the government so that the private firm can develop it. This requirement is stipulated in Regulation of Minister EMR Number 28 Year 2012 (supplemented with Regulation of Minister EMR 07 Year 2016).

These regulations bar the entrance of private utility that can offer green electricity to segmented markets. With the rise of electric vehicles in Indonesia, there are lots of people who are really eager to use green electricity, including from floating solar PV.

- Unattractive tariff and business scheme for IPP

The second option besides private utility is Independent Power Producer (IPP). IPPs in Indonesia face several challenges and unattractive aspects related to the regulatory and business environment, which can make it less appealing for foreign and domestic investors. Some of the key unattractive elements of the climate for IPPs in Indonesia include unattractive scheme and tariff issues, among others.

All small-medium scale renewable developers that have signed PPAs with PLN in the period 2017-2021, failed to realize their projects. The reason is that the PPAs signed are PPAs designed by PLN and PLN does not want a "take or pay" clause in the PPA, thus causing great uncertainty for financiers who will finance the plant and the developer.

- Tariffs

Indonesian government has a significant role in setting electricity tariffs, which may not always align with the cost of production. In some cases, tariffs may be kept artificially low for political reasons, affecting the financial viability of projects. The latest regulation that oversees electricity selling price from IPP to PLN is Presidential Decree No. 112/2022 (tariff scheme of this regulation is described in section IV). Despite the push to have feed-in tariff (FIT) for renewable energy power plant from industry players and investors, the government has decided to introduce new ceiling tariff that varies depending on the types of renewable energy power plants and its location. The concept of ceiling tariff is not much different from what is applied under PLN’s Generating BPP scheme. Under the ceiling tariff scheme, the tariff offered and negotiated between an IPP and PLN must not be higher than the ceiling tariff for that particular type of renewable energy power plant, which is derived from the tariff set out in the appendices of PR 112 multiplied by the relevant location tariff. The difference with the Generating BPP’s scheme is that the ceiling tariff for renewable energy power plant is no longer benchmarked against the Generating BPP for non-renewable energy such as coal, which is cheaper. The basis for the tariffs set out under PR 112 is unclear and does not deviate from the tariffs that were applied to successful renewable energy projects in Indonesia in general.

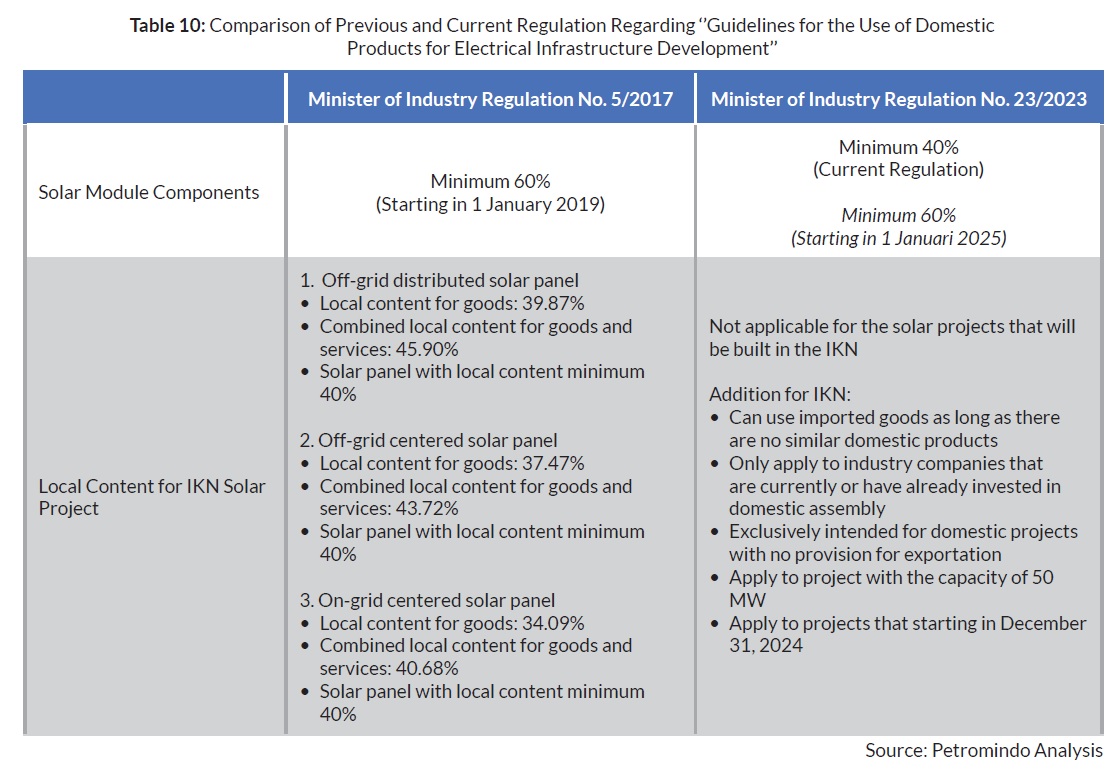

IV.2 Local Content Requirement (TKDN) Regulation Alteration

Based on the previous Minister of Industry Regulation No. 5/2017, from January 1, 2019, the minimum Domestic Component Level (TKDN) value for solar panel module components had to reach at least 60 percent. In fact, the actual TKDN value for solar panel modules currently averages only 47.5 percent.

For example, Fabby Tumiwa, Chairman of the Indonesian Solar Energy Association (AESI) said that the Cirata FSPP project was delayed due to the length of time to arrange waivers for the use of imported or non-TKDN solar modules. According to industry players, it takes around 7 months to complete the waiver processing process from the Ministry of Industry.

But based on the new Minister of Industry Regulation No. 23/2023, the TKDN value will change to a minimum of 60 percent starting January 1, 2025. In addition, there are exceptions for the construction of FSPP in IKN, which include, being able to use imported goods as long as there are no similar domestic products, applies to projects with a capacity of 50 MW that have been assigned the implementation of electricity infrastructure development for the core area of the IKN government center, and are valid for projects that start commercial operations no later than December 31, 2024. An additional note for these imported goods is that they can only be carried out by solar module industry companies that are and/or have invested in domestic assembly and only to meet domestic electricity supply requirements.

Based on our analysis, for solar panel development companies in Indonesia, achieving a TKDN value of 60 percent is a challenge. This is a very optimistic target. However, companies can still prepare approximately 2 years to meet the TKDN value. On the other hand, with the current TKDN value, which is 40 percent, most companies still find it difficult to fulfil it. This is because the cost of producing solar modules in Indonesia is much more expensive than importing from other countries. The high production costs are caused by expensive imports of raw materials and assembly costs. If we compare to China, the cost of producing solar modules is 20-30 US cents per Wp, while in Indonesia, the cost reaches US$1 per Wp.

For IKN itself, the 50 MW capacity allocation for solar panels represents great potential for development companies. However, the problem is that before developing solar panels in IKN, the company must build solar panel facilities in other areas in Indonesia.

• Water Quality Decline Potential Effect

The existence of FSPP has the potential to affect the quality of water bodies from reservoirs. The FSPP that will cover the dam certainly has the potential to reduce the amount of solar radiation entering the water's surface. This phenomenon causes increased stratification, namely the formation of layers of water based on temperature, thus limiting the mixing of water under and around the installation which can reduce dissolved oxygen levels in the water. This decrease in dissolved oxygen levels has the potential to affect the quality of life of the biodiversity that lives in that place. The magnitude of the increase in stratification will depend on the location and scale of the plant (the ratio of the covered area of the water body to the total area of the water body). The smaller the ratio, the less significant the impact on water quality will be.

V. Opportunities in Indonesia

• Lower Investment Cost Compared to Other Types of Solar Power Plant

Investment value required to develop FSPP in Indonesia is a minimum of US$0.59 million per MW. If we compare it with the minimum investment value to develop other types of solar power plants, such as rooftop solar power plant which is US$0.98 million per MW and ground-mounted solar power plant which is US$0.87 million per MW, we can see that FSPP has succeeded in being superior to these two types of solar power plant. This can certainly open up opportunities for companies that want to develop FSPP.

Based on Table 12, we can see that the average investment cost for developing FSPP also varies, depending on several factors, such as project capacity, wave intensity, salinity level, weather conditions, grid infrastructure, and access to the development site. The greater the project capacity, the presence of grid infrastructure, the ease of area coverage, then the wave level, wind speed, low water salinity, then of course it will have an impact on lower investment costs, and vice versa. These factors can be taken into consideration for business actors to choose the right location in developing FSPP in Indonesia.

• Raw Material Availability in Indonesia

There are 3 main materials for producing solar panels, namely high-density polyethylene (HDPE), galvanized steel, and aluminum. Based on our analysis, one of the materials that is abundant in Indonesia is bauxite, which is the raw material for making aluminium, which is one of the materials for making solar panels.

The estimated total aluminum production capacity in Indonesia until 2029 is projected to reach 3.9 million tons per year. On the other hand, the current demand for aluminum in Indonesia is around 1 million tons per year. Thus, there will be a surplus supply of aluminum produced in Indonesia in 2029. Apart from the potential for export, we see the potential for using domestically-produced aluminum as a raw material for making solar panels.

This is in line with Xinyi Solar Energy's plan through Xinyi Glass to build a solar panel factory on Rempang Island, Batam, Riau Islands with an investment of US$11.5 billion and SEG Solar Inc.’s in Batang, Central Java with an investment plan of US$500 million (Petromindo, 2023). It is very possible that the aluminum supply needed by the factories will be sourced from domestic aluminum smelters. Of course, besides being able to meet the required TKDN value, aluminum smelter entrepreneurs can also find a domestic market for their aluminum products.

• TKDN Alteration from Potential of Solar Panel Factory in Indonesia

Behind the challenges related to TKDN in the development of FSPP in Indonesia, a glimmer of hope can be seen from the plan to develop a solar module manufacturing factory that will be carried out in Indonesia, namely US-based SEG Solar Inc. which is a company that is collaborating with ATW Group to develop a solar module factory with a capacity of up to 5 GW and an investment value of US$500 million in the Batang Industrial Area, Central Java. Apart from that, China-based Xinyi Solar Energy, through Xinyi Glass, also plans to develop a solar module factory with an investment value of US$11.5 billion on Rempang Island, Batam, Riau Islands (Petromindo, 2023). These planned two projects show that Indonesia has the potential to produce materials used for FSPP. If the material comes from 100 percent domestic factories, issues related to challenges in fulfilling the TKDN value for FSPP should not be a lasting problem once the factories are already in operational.

• Solar Power Plant Electricity Price Decrease

Based on our analysis, opportunities that can be obtained to accelerate the development of FSPP in Indonesia, we can see from the decline in the price of solar power plant electricity obtained through power purchase agreements (PPA) entered into by PLN with private electricity developers. Between 2015 and 2022, we can see that the solar power plant's PPA price has decreased quite significantly, which is by 78 percent, from US$0.25 per kWh to US$0.056 per kWh.

Chapter VI. Existing and Planned Floating Solar Power Plants in Indonesia and Chapter VII. Industry Contacts, are available in report's PDF, that can be downloaded here.

Petromindo Research

Inquiry: research@petromindo.com